A decade ago, LIBOR- the London Interbank Offered Rate was the most crucial benchmark for determining the interest rates on consumer and commercial loans. However, it was villainised and doomed due to multiple scandals and being a key factor in the 2008 financial crisis.

The Secured Overnight Financing Rate(SOFR) is the replacement for LIBOR in the United States. Similar to LIBOR, the SOFR is a benchmark used by financial institutions to price loans for consumers and businesses.

Previously, LIBOR was the go-to benchmark to determine the interest rates at which investors and banks gave out loans. It comprised five currencies and seven maturities and was determined by calculating the average interest rate at which global banks borrow from one another.

However, following the 2008 financial crisis, regulators understood that they relied too much on LIBOR. In a short while, it was replaced by the Secured Overnight Financing Rate(SOFR).

In this blog, we will explain what is SOFR, the difference between LIBOR and SOFR, and how can it affect you.

- What is the Secured Overnight Financing Rate(SOFR)?

- How Does SOFR Work?

- Why did SOFR replace LIBOR?

- Difference Between LIBOR and SOFR

- Advantages and Disadvantages of Secured Overnight Financing Rate

- What is the SOFR Rate Today?

- Other Alternatives to LIBOR

- Transitioning to SOFR: What Does it Mean For You?

- Final Words

- Frequently Asked Questions(FAQs)

What is the Secured Overnight Financing Rate(SOFR)?

The Secured Overnight Financing Rate is a benchmark used by financial institutions and banks to determine the interest rate for dollar-denominated derivatives, and consumer, and business loans. It replaced the London Interbank Offered Rate in June 2023. According to experts, the implementation of SOFR offers fewer opportunities for market manipulation and current rates instead of forward-looking interest rates and terms.

The term ‘overnight financing’ in the name is a reference to how SOFR sets rates for lenders. It is based on the interest rates that financial institutions pay each other for overnight loans.

LIBOR was based on interest rates that the financial institutions said they would offer each other for short-term loans. On the other hand, SOFR provides a solid and transparent method to identify a common benchmark rate based on observed transactions in the marketplace. SOFR takes into account actual lending transactions between institutions, making it more reliable.

Other countries have their own overnight rates like SONIA in Great Britain’s Sterling market or the Euro Overnight Index Average(EONIA) in Europe.

How Does SOFR Work?

Large financial institutions loan money to each other using Treasury bond repurchase agreements, which are also called ‘repos.’ The repo agreements allow banks and financial institutions to make overnight loans to meet their reserve and liquidity requirements by using Treasury as collateral.

Secured Overnight Financing Rate comprises the average of the rates charged in repo transactions. Every morning, the New York Federal Reserve Bank publishes the SOFR rate it has calculated for repo transactions on the previous day from the three markets-

Tri-party Repo Market: It comprises three major parties- securities dealers, cash investors, and clearing banks that function as intermediaries between dealers and investors(money market mutual funds, lenders, securities, etc.) in the repo transaction.

General Collateral Finance(GCF) Repo Market: Collateralized repurchase agreements in which the assets pledged as collateral are not specified until the end of the day.

Bilateral Repo Market: These are transactions in which asset managers and institutional investors borrow securities from brokers or securities lenders either on a bilateral or cleared basis in the absence of a clearing bank but are instead cleared by the Fixed Income Clearing Corporation.

Let’s understand the application of SOFR through an example.

Suppose a bank has an average daily cash requirement of $50 million to cater to its customers and all the branches in the city. On 9th November, they were left with a cash reserve of $30 million at the end of the business hours.

In order to meet its liquidity and reserve requirements, they took out an overnight loan from ABC bank for $20 million, for which they produced government bonds held as collateral. The next day, the 10th of November, the first bank will return the money to ABC Bank with the SOFR rate determined by the New York Federal Reserve.

Why did SOFR replace LIBOR?

Ever since the 1980s, LIBOR has been the major benchmark for loan rates. However, after the financial crisis of 2008, it got a bad reputation and was associated with multiple scandals. The financial crisis of 08 revealed various technical shortcomings of LIBOR. Investors and banking regulators were aware that a new permanent alternative to LIBOR was needed.

These scandals were partly driven by the interbank lending market diminishing in recent years. With fewer transactions, the index started reflecting quoted rates instead of actual rates from transactions. This self-reported rate from LIBOR may not accurately represent the cost of borrowing.

Unlike LIBOR, the Secured Overnight Financing Rate is much less likely to be manipulated than the Treasury repo market is one of the most liquid markets in the world, meaning there’s more real transactional data to rely on, instead of self-reported rates.

The SOFR market averages $1 trillion per day, meaning it reflects actual transactions, not quotes. This makes it harder to manipulate.

Difference Between LIBOR and SOFR

Since LIBOR and SOFR are typically used for the same purpose, let’s understand the difference between LIBOR and SOFR.

| Parameters | SOFR | LIBOR |

| Function | SOFR is a benchmark used to determine the interest rates at which financial institutions lend overnight loans to each other. | LIBOR is a benchmark used to calculate the interest rate of a loan from one day to twelve months based on the estimated borrowing rates that are levied on their borrowing counterparts. |

| Collateral | Collateralized with treasury security | It is an unsecured loan. No collateral is required for financing. |

| Period | It can be used as an interest rate only for an overnight transaction. The interest rates are published daily based on the previous day’s transactions. | LIBOR’s interest rates are calculated according to a timeline ranging from overnight to up to twelve months. |

| Manipulation | Since the rates are based on the previous day’s transactions and the credibility of the institution publishing the rates, SOFR is less prone to unethical and fraudulent activities. | Since LIBOR is determined by the average estimate of the bank’s borrowing rates and can apply for periods of up to a year, it is more prone to unethical activities and manipulation. |

A key difference between LIBOR and SOFR is that the former is based on quotes from reporting banks not required for financial transactions and the latter is based on completed financial transactions.

Another major difference is that while Libor was forward-looking, SOFR is backward-looking. This means that LIBOR banks knew what the interest rates were at the beginning of the period. However, with SOFR, the borrower won’t know exactly what they owe until the end of the loan.

Moreover, LIBOR is an unsecured loan, meaning it doesn’t require any collateral, thereby including a credit risk premium. SOFR is a secured rate, based on transactions that involve collateral in the form of treasury, meaning no credit risk premium is involved.

Read Also:- When is the Next Fed Meeting? What Can You Expect?

Advantages and Disadvantages of Secured Overnight Financing Rate

Although SOFR came into place due to the replacement of LIBOR, there are still a fair share of pros and cons.

Advantages of SOFR

Credibility: Since the Federal Reserve Bank of India releases the SOFR rates daily, it has certified the credibility and genuineness of such rates. In fact, the New York Federal Reserve Bank is next in line with the top banks in the United States banking system.

Free from Manipulation: Since the rates of Secured Overnight Financing Rate are based on actual transactions, there is little to no chance of manipulation, compared to LIBOR.

Resilience: SOFR is more resilient than LIBOR, owing to the process of how the rates are derived and the liquidity and depth in the underlying markets.

Disadvantages of SOFR

Liquidity: Since the loans under LIBOR are still undergoing, comparing the two options displays a significant difference in their liquidity rates. The LIBOR system offers more liquidity than the SOFR.

Period: As mentioned above, SOFR is an overnight, meaning it provides interest rates for a limited time frame. However, LIBOR is a benchmark that borrowers and investors can use to determine the interest rates for the next 12 months.

Applicability: Besides the derivatives market, the applications and use of SOFR is quite limited, like in the case of the cash or currency market.

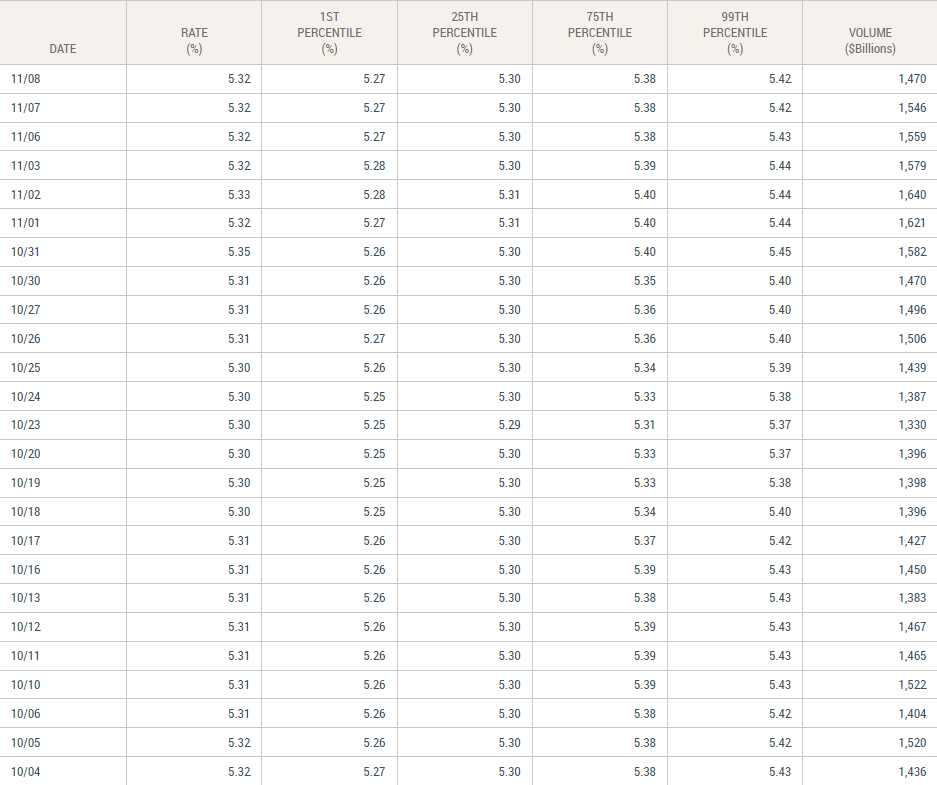

What is the SOFR Rate Today?

By now, you must be wondering what the SOFR rate is today. Lucky for you, the New York Fed publishes the rates publicly on its website.

Source: New York Fed

Other Alternatives to LIBOR

While SOFR has been making the headlines as the replacement for LIBOR, there are other options out there. Other alternatives used in the United States and all over the world include-

Sterling Overnight Index Average(SONIA): SONIA replaced LIBOR in the United Kingdom in 2021. It is administered by the Bank of England and reflects the average rates for overnight UK Pound-denominated loans among banks and financial institutions.

Federal Funds Overnight Index: The federal funds rate is what U.S. banks pay each other for unsecured loans from their reserves. The index of these rates may also be used to replace LIBOR by specific lenders.

Ameribor: Developed by the American Financial Exchange(AFX), Ameribor is an index based on the unsecured loan costs of medium and small-scale banks across the United States. The data is stored on the blockchain and the index is created by a credit-weighted average of the involved unsecured loans.

U.S. Prime Rate: The prime rate has been used for years as a threshold for setting credit cards, home equity lines of credit, and other Annual Percentage Rates(APRs). It is partially based on the federal funds rate.

Read Also:- Top 10 Financial Mistakes to Avoid

Transitioning to SOFR: What Does it Mean For You?

On November 30, 2020, the Federal Reserve announced that the LIBOR system would be replaced by SOFR by June 2023. Federal banks and financial institutions were also instructed to stop writing contracts using the LIBOR system by the end of 2021.

According to experts, the average consumer or investor should not notice any change during the shift from LIBOR to SOFR. The change will mostly affect financial institutions. However, if you look at interest rates, you will find a notation that they are calculated by SOFR, instead of LIBOR.

Borrowers looking for adjustable-rate mortgages are already witnessing SOFR prices, and this trend will continue to grow across other types of adjustable-rate consumer products. That being said, it will take some time for current LIBOT borrowings to work through the system. As a result, existing LIBOR contracts will still be a part of the financial landscape till the end of their tenure.

Transition Challenges

The transition to SOFR from LIBOR is expected to majorly affect the derivatives market. But, it should also play a crucial role in consumer credit products, including adjustable rate mortgages, debt instruments like commercial paper, and student loans.

In the case of adjustable-rate mortgages based on the Secured Overnight Financing Rate, the movement of the threshold will determine how much borrowers will pay once the fixed interest period of their loan ends. If the SOFR is higher at the end of the loan tenure, borrowers will be paying a higher rate.

Final Words

The Secured Overnight Financing Rate(SOFR) is the benchmark for interest rates on dollar-denominated derivatives and loans. It replaced the London Intrabank Offered Rate in 2023, which was the globally accepted benchmark before SOFR. The Secured Overnight Financing Rate reflects an overnight rate whereas the LIBOR is a forward-looking rate, making SOFR less prone to manipulation and market fluctuations.

The transition to SOFR from LIBOR represents a huge change in the inner workings of the global financial system. Although LIBOR system loans are still functioning at present, they will certainly become less visible in the coming years.

Read Also:- Stock Market Crash: What Happens to Your Money When the Market Crashes?

Frequently Asked Questions(FAQs)

Ans. The Federal Reserve does not publish a 3-month SOFR rate. However, the Chicago Mercantile Exchange publishes one-, three-, six-, and 12-month term SOFR rates for the derivates market.

Ans. SOFR measures the cost of overnight borrowing, using Treasury securities as collateral. Banks used to follow the LIBOR system to borrow from each other intentionally. The replacement of the LIBOR system was announced on Nov 2020 and it was completed on June 2023.

Ans. According to the New York Federal Reserve Bank, the Secured overnight financing rate today is 5.32%.